Advantages of Kisan Vikas Patra: Kvp is a one-time investment scheme of the Government of India, where your money doubles in a given period. Kisan Vikas Patra is present in all post offices and big banks of the country. Its maturity period is still 124 months. The minimum investment in this is 1000 rupees. There is no maximum investment limit. Government guarantee is available on post office schemes, that is, there is no risk at all.

If you like this article then please like us on Facebook so that you can get our updates in future ……….and subscribe to our mailing list ” freely “

Quick Links

Key Features of Kisan Vikas Patra (as of 2025):

| Feature | Details |

|---|---|

| Issuer | India Post (Department of Posts, Govt. of India) |

| Eligibility | Indian citizens (18+ years), can be purchased individually or jointly |

| Minimum Investment | ₹1,000 (and in multiples of ₹100) |

| Maximum Investment | No upper limit |

| Interest Rate | ~7.5% (compounded annually, changes periodically) |

| Maturity Period | 115 months (9 years and 7 months) |

| Maturity Amount | Investment doubles at maturity |

| Taxation | No tax benefits under Section 80C; interest is taxable |

| Premature Withdrawal | Allowed only after 2.5 years (under certain conditions) |

| Nomination Facility | Available |

| Transferability | Can be transferred from one person to another or between post offices |

Advantages of Kisan Vikas Patra

- The interest rate in this scheme is 7 percent, which is more than the bank’s FD.

- It can take advantage of 1000 rupees. At the same time, there is no fixed amount of investment.

- This is a post office scheme, so there is no money to sink money.

- You can buy this scheme from any post office.

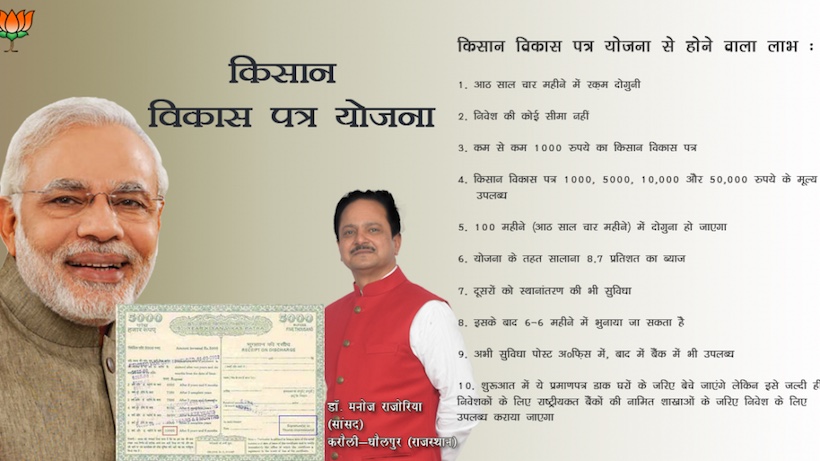

किसान विकास पत्र के फायदे

- इस स्कीम में ब्याज दर 7 फीसदी तक है जो बैंक एफडी से ज्यादा है।

- इसका फायदा 1000 रुपए से ही ले सकते हैं। वहीं, निवेश की कोई अधिकतम राशि तय नहीं है।

- ये पोस्ट ऑफिस की स्कीम है ऐसे में पैसे डूबने के चांस भी नहीं है।

- इस स्कीम को आप किसी भी पोस्ट ऑफिस से खरीद सकते हैं।

1. Highly secured :

The main advantage of the many Kisan Vikas Patra is that, being a Government scheme that encourages small investors to do savings, it is completely secured. Small investors who are extremely concern about security for their investment can opt to invest in Kisan Vikas Patra.

2. Flexibility in terms of amount :

One can habituate savings by buying KVP of the lowest value i.e. Rs. 100. KVP is available from Rs. 100 to Rs. 50000 face value. The value that the investor will receive on completion of eight years and seven months is declared on the KVP itself. Thus they can know the maturity amount at the time of inception of their investment itself.

3. Can use as Collateral security :

Many banking companies and financial institutions, Non-banking companies accept KVP as collateral securities. So they can be used as a highly liquid property.

Must Read – National Pension Scheme

4. High security for acting as Negotiable instruments

The benefits of Kisan Vikas Patras can be availed by the holder of the KVP since KVP is issued in the name of the holder and cannot be transferred to others without completing the required legal formalities. To get the KVP transferred on to the name of any other person permission of the authority where it was obtained is required.

5. Formalities are nominal :

No complex formalities are there in obtaining Kisan Vikas Patras when compared to other type of financial instruments. And financial literacy is also not required any more.

6.Pre mature withdrawal is available so that in case of any urgency the Patras can be encashed very easily ….so they are highly liquid instruments.

How to open account?

- You can open an account by going to any post office and filling the form. The form can also be downloaded online.

- The full name, date of birth and address of the nominee should be written on the form.

- The amount of purchase amount must be clearly written in the form.

- The amount of KVP form can be paid through check or cash.

- If you are paying through check, write the check number information on the form.

- Explain in the form KVP single or joint ‘A’ or joint ‘B’ membership, on what basis is being purchased.

- Write the names of both the beneficiaries on joint purchase.

- Write the date of birth (DOB) of the beneficiary, name of the parents, if the beneficiary is a minor.

- On submitting the form, a farmer development certificate will be given along with the beneficiary’s name, maturity date and maturity amount.

1000 के मल्टीपल में जमा करना होंगे रुपए

इस स्कीम में 1000 रुपए के मल्टीपल में रुपए जमा करना होते हैं। यानी 1000 रु, 2000 रु, 3000 रु या फिर इसी तरह कोई अन्य अमाउंट। आपको सारा पैसा एक बार में ही देना होगा। यानी इसमें हर महीने या साल में पैसे जमा करने का सिस्टम नहीं है। जैसे आपको 1 लाख रुपए के 2 लाख करने हैं, तो इसके लिए आपको पूरे 1 लाख रुपए स्कीम लेते समय जमा करने होंगे, जो 9 साल 10 महीने के बाद 2 लाख रुपए बन जाएंगे। पोस्ट ऑफिस द्वारा इस अकाउंट के लिए पासबुक भी दी जाती है।

मेच्योरिटी से पहले निकाल सकते हैं पैसे

- किसान विकास पत्र स्कीम से आप इमरजेंसी के वक्त अपना फंड मेच्योरिटी से पहले वापस ले सकते हैं, लेकिन 2.5 साल होना जरूरी है।

- मेच्योरिटी से पहले पैसा निकालने पर उस पर तय इंटरेस्ट से 2 फीसदी घटाकर पूरा अमाउंट वापस मिल जाएगा।