Sometimes the bank refuses to give loans or credit cards even to those people who have a thick salary or good business. Then when the bank is asked the reason, the answer is that your Cibill Score is not good or is negative. A CIBIL score is a three-digit number (ranging from 300 to 900) that indicates your creditworthiness—how likely you are to repay a borrowed amount, based on your credit history. It is issued by TransUnion CIBIL, one of the leading credit bureaus in India.

Actually, in this world of digital transactions, facilities are now available online. All the transactions that you do with the bank are seen while taking the loan. Often, the bank offers the loan to the customer only on the basis of credit score. If your credit score is good, then banks will not shy away from giving you a loan.

When you apply for a loan in banks, the banks check your credit history whether you have ever taken a loan before or if you had taken a loan, if it was paid at the time. The bank comes to know through the CIBIL score that you have made a mistake in the past, only then the bank refuses to give the loan.

Quick Links

What is CIBIL score?

Credit Information Bureau India Limited (CIBIL) is a company that maintains a record of every loan i.e. maintains a complete account. The CIBIL is judged on the basis of the Credit Information Report (CIR). In this report, there is complete information about loan and credit cards taken by you. How do you use the loan EMI and credit card and pay their bills. Your credit score is generated on that basis.

Due to poor CIBIL score,

people often do not pay at the right time by taking a loan. Filling of EMI late, not paying the credit card on time, such a step adversely affects the CIBIL score. Apart from this, making a lot of inquiries about the loan also has a negative impact on the CIBIL score, because all the banks you contact will check the CIBIL score. Due to frequent CIBIL checks, it has a negative effect.

How to improve the CIBIL score

in one line, pay any loan on time. Maintain the balance in the use of home loan, auto loan, personal loan and credit card. Excessive dependence on one type of credit can damage your score

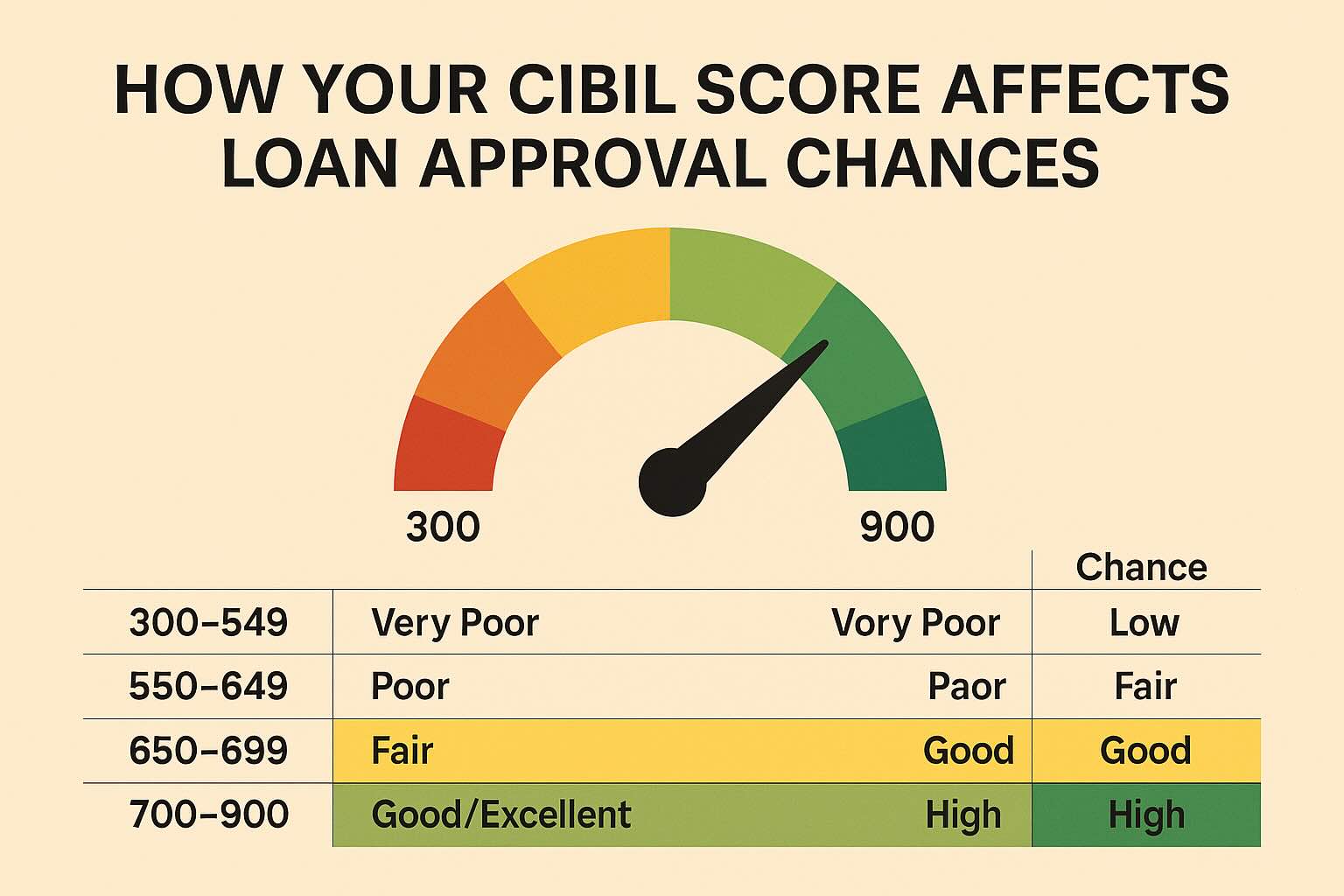

A credit score or CIBIL score is a 3-digit number. It can be between 300 and 900. Your civil score is closer to 900, it is considered as good. That is, the higher the better. Based on this, banks decide how much loan should be given to you. About 79 percent of the loans are given by looking at the CIBIL score of more than 750.

Rating means that

- 750–900 → Excellent (high approval chances)

- 700–749 → Good (likely to get loans with favorable terms)

- 650–699 → Fair (may get loans but with higher interest)

- 550–649 → Poor (low approval chances, high interest)

- 300–549 → Very Poor (loan applications often rejected)

if a customer has a CIBIL score between 300 and 550, then it is considered a puerile, and the bank refuses to give loans directly to such customers. If the CIBIL score is between 550 and 650, it is considered average. In such a situation, the bank may refuse to give a higher rate of interest or loan. At the same time, if it is between 650 to 750 then it is considered good and the bank will consolidate the loan. On the other hand, if the customer’s CIBIL score is between 750-900, then the bank will offer the loan at the lowest interest rate without delay.

The better your credit score. You will be more likely to get your loan from banks. Therefore, an effort should be made that the CIBIL score is not below 750.

Where to know:

How much is your credit score. You can easily find it in a few seconds. In this, you can take help of State Bank of India. For this, go to https://homeloans.sbi/. Personal details have to be entered here. PAN number or any identity card details will have to be given here. You will also have to enter mobile number and email id here. As soon as you give all these details, you will get an OTP on the mobile number. After entering this OTP, your credit score will be visible in front of you.