Venture Capital Pricing Game: How do Venture Capitals (“VCs”) attach numbers to companies? Valuing companies at conventional DCF models often churns out values half or a third of what the VCs value them at. So why does the difference arise? The standard response is that VCs don’t value companies – they price them.

There’s a difference in the pricing process and the value process. Classrooms, books, and all educational media spend a lot of time explaining the factors that drive the value process such as cash flow, growth, and risk. We often use DCF as the tool to arrive at the value. The pricing process on the other hand is driven by demand and supply. The price and value may be the same in an efficient market.

We understand from behavioural studies that the pricing game factors in mood, momentum, liquidity, small pieces of information, and other softer issues that drive markets. Pricing is often based on multiples and comparables rather than discounted cash flows. Going a step further, the pricing process can even be studied on charts and technical indicators.

So how do VCs price a company? There’re 3 fundamental ways

Quick Links

1. Recent Pricing by another VC

VCs first establish a baseline price by the most recent investment by another VC in the same company. They might spend an amount higher or lower, but that becomes the benchmark of the price they pay for the company today. This is not just for new investors but for existing investors as well for marking up (or down) their investments. The dangers are manifold. They’re just looking at one company and one investment which means one bad investment can open a feedback loop and hijack transactions for the foreseeable future. A few people start (or stop) throwing money around and the pricing process can get out of control very quickly in either direction.

2. Pricing of other private companies

This is an extension of the above where VCs look at similar companies. The problem with this approach is that the word “similar” is very subjective. VCs decide the “similarity” on the basis of size, sector, geography, macroeconomic cycles, etc. and scale the prices for some common metric. For example, in case of cab companies like Ola, Ubers, Meru, etc. the pricing is scaled relative to the number of riders or the number of drivers or geographical spread.

3. Pricing of public companies

This is used for companies that already have substantive revenues and profits. Here you can compare the subject company with companies listed on the stock exchanges.

3.2. Pricing of public companies + Forecasting

Most young start-ups don’t have much revenues or profits today. So sometimes VCs forecast the earnings of these companies to 3-5 years or as many years as it takes to get profits, apply the current multiples of public companies to the subject company, and discount the price back to the present value using a target rate of return. The target rate of return is the reflection of the confidence in the company. Most young start-ups do not make it and this needs to be reflected in the target rate of return.

So VCs price companies just like public markets do. The difference is in statistics. There’re a thousand listed oil companies in the world but maybe ten cab companies, all unlisted. So the VCs have a much smaller sample size. Within that sample space there’s no 24/7 trading but 2-4 transactions a year so there’s infrequent updating of prices. In addition, the transactions themselves have options embedded in them which do not reflect in the numbers. Some options allow the VCs special prices on future capital raising. So ? 1 million for 10% of a company does not necessarily value it at ? 10 million if there’re enough options in the pricing, but that’s what the newspapers miss to report.

Must Read – Venture Capital Finance

Another problem with VC pricing is that they generally lag the markets. It is a common observation that there’re lots of VC transactions when the economy is booming which can virtually dry up during recessions. When the transactions stop, so does the repricing and we see the VC returns lagging the market by 1-2 quarters if there’s not enough repricing being done.

There is a lot of lot of value locked up in unrealized returns of VC investments. Unlike market investments like mutual funds where the returns are calculated by the realized returns (dividends and capital gains) and the market value of the investments, VC investments are more difficult to monetize. They aren’t based on market prices but rather on estimates. These estimates are often based on what other VCs are paying for similar companies. There’s also a lot of noise and bias in the data available while valuing VC funds. So, they cannot be measured like market investments.

Finally, VC investments are very difficult to liquidate. There’s a long time horizon involved. VCs take a position in an undeveloped company, build-up the company, and find someone who will be willing to take it off your hands at a much higher price.

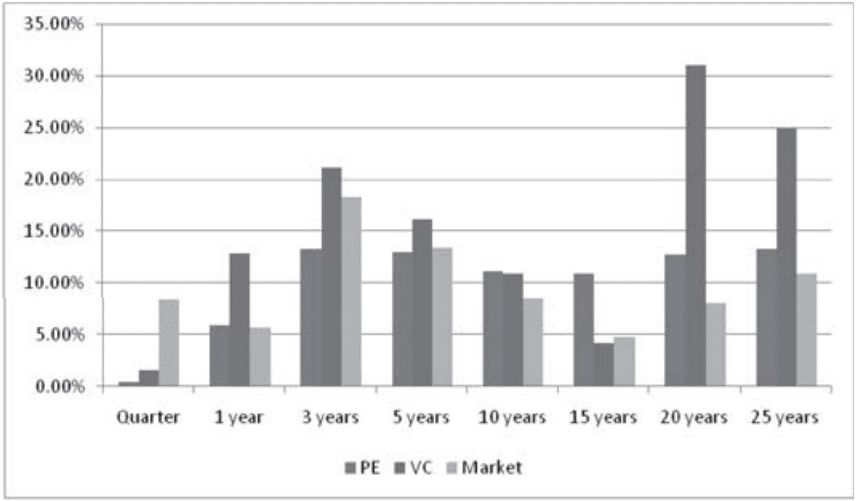

All these issues might make VC investment look problematic. But across time, VCs have done much better than PE investors and index funds, which are a proxy for public market investors. So surely, VCs bring something to the table that public and private investors do not.

Must Read –